|

|

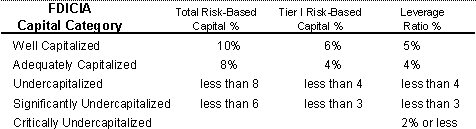

Risk-Based Capital Standards

|

|||||

|

|

|

The regulatory capital category that your bank falls under can have

significant impact on your ability to run your bank. The provisions for

capital based supervision, as established by FDIC Improvement Act (FDICIA),

are summarized here.

"Well Capitalized" banks are the only ones that escape required regulatory sanctions. "Adequately Capitalized" banks are prohibited from accepting brokered deposits without the prior approval of the FDIC, and may not pay interest "significantly above prevailing interest rates" on any deposits. "Undercapitalized" banks are subject to all of the restrictions of adequately capitalized banks, must also submit acceptable capital restoration plans to the appropriate federal banking agency (including a parent company guarantee of compliance in the case of a bank holding company subsidiary), are prohibited from paying dividends or paying management fees to a parent bank holding company, cannot increase total assets, and are limited in their ability to make acquisitions, open new branch offices, or enter new lines of business. "Significantly Undercapitalized" banks are subject to the same restrictions as undercapitalized institutions, may not pay a bonus or give a raise to a senior executive officer without prior regulatory agency approval, and may also be required, among other things, to raise additional capital, reduce total assets, terminate certain activities, replace officers or directors, or seek to be acquired. "Critically Undercapitalized" banks must be closed or placed into conservatorship unless good cause to do otherwise exists, and if allowed to survive are to be subjected to an even broader array of operating restrictions. Additionally, at each lower level of capital, the premiums for FDIC deposit insurance coverage increases.

|