|

4th Quarter 2002 |

Higher Interest Earnings at Risk

|

||||

|

|

Here we go, again. Last quarter we observed, that despite the historically high levels of core

deposit funding, many community banks still had elevated levels of

short-term interest rate risk. Last quarter we observed, that despite the historically high levels of core

deposit funding, many community banks still had elevated levels of

short-term interest rate risk.

We evaluate short-term interest rate risk by Net Interest Earnings at Risk (or Margin at Risk). To measure this we take a one-year forecast of interest earnings, and use it as a base amount. Then run two additional simulations: one shocking rates up and the other shocking rates down. The simulation, up or down, that produces the most negative change to the base net interest earnings, defines the amount of potential risk. So what is the continuing trend we see for community banks? Throughout the very dynamic interest rate decline, the level of Net Interest Earnings at risk has continued to increase. Over the past 2 years the average Net Interest Earnings at Risk has increased from ¢4.66% in December 2000 to -7.66% by December 2002. Margins are off

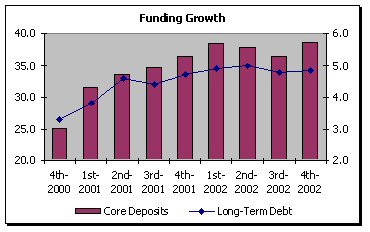

While all banks have experienced such increases, the trend is most noticeable at the nationÆs largest institutions. For the largest banks the level of interest bearing core deposits as a percentage of assets grew from 25.13% in December 2000, to 38.60% in December 2002. Historically low rates have also prompted bankers to examine alternative sources of funding. Funding from the FHLB and other sources has become much more attractive given the current interest rate environment. Many banks are beginning to take advantage of lower fixed rate funding. On average, as a percentage of assets, long-term debt rose from 3.28% in December 2000 to 4.84% by December 2002. Increased Risk If rates fall, banks will have a hard time lowering core deposit rates further. These rates are already at historic lows. Currently Bankrate.com reports the national average for Interest Bearing Checking accounts to be less than 0.80% 2. As market rates decline, asset yields have more room to drop than funding rates, therefore margins could compress even further. Falling rates would also be bad news for those banks that choose to lock in todayÆs low rate funding. Obviously, securing a fixed rate on long-term debt would have a negative impact on margin if rates continue to drop. Actually, this is exactly what the interest rate risk peer data shows. The increase in margin at risk over the past 8 quarters has been driven mostly by an increase in risk to down rates. Earnings at Risk Given Down Rates has gone from +2.24% in December 2000 to ¢7.07% by December 2002. The measurement starts out positive, meaning that initially, banks benefit from falling rates. However the measurement quickly turns negative by mid-year 2001, indicating that banks should expect margins to decline when rates fall. Looking for a rate increase Most banks are poised for a rate increase. But will we see that any time

soon? With the lackluster economy, and our country at war, itÆs hard to

tell. When the Fed last met in March, they acknowledged that the economy was

in a ōsoft-spotö and that given world events they will wait and see if

further rate cuts are needed. Further rate cuts would not be good news for

community banks. 1 FDIC, Quarterly Banking Profile, Fourth Quarter 2002

available at www.fdic.gov

|

|

This

A/L BENCHMARKS Industry Report article was published |

Balance sheet trends continue

Balance sheet trends continue So do higher levels of core deposits and an increase in long-term

fixed-rate funding add up to more interest rate risk? The answer is yes, if

rates continue to decline.

So do higher levels of core deposits and an increase in long-term

fixed-rate funding add up to more interest rate risk? The answer is yes, if

rates continue to decline.  No crystal ball is 100% accurate, so itÆs hard to tell precisely what effect

a change in rates will have. It seems clear that banksÆ net interest margin

will decline further if rates continue to drop. Since March 2002, the number

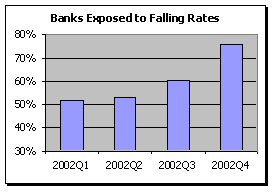

of banks at risk to falling rates has increased from 52% to 76 %.

No crystal ball is 100% accurate, so itÆs hard to tell precisely what effect

a change in rates will have. It seems clear that banksÆ net interest margin

will decline further if rates continue to drop. Since March 2002, the number

of banks at risk to falling rates has increased from 52% to 76 %.