|

3rd Quarter 2002 |

Where will margins go from here?

|

||||

|

|

|

Changes… To say that the banking industry has weathered significant changes over the past two years is an understatement. The interest rate environment has been very dynamic and consumer confidence has been shaken. Both have had a significant impact on a community bank’s balance sheet and its interest rate risk position.

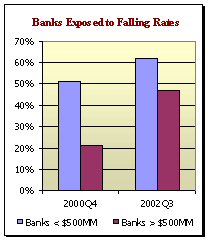

Another big change has been the erosion in consumer confidence. The aftermath of the tech-stock boom coupled with the questionable accounting practices of some large public companies, has driven the average investor away from mutual funds and the stock market, back to more traditional savings vehicles. Impact on the balance sheet… I Normally an increase in the level of core deposits helps a bank stabilize its Margin at Risk. These types of deposits typically have administered rates (rather than market rates). Therefore banks can more easily control their level of exposure. As rates rise a bank may not raise its core deposit rates as quickly thereby limiting the increase to its interest expense. If rates fall, banks generally drop their core deposit rates to match the changes in the market. In either case, a bank usually has a good tool to mitigate their short term IRR. The problem is that rates are already at historic lows. Institutions are having a much harder time lowering these administered rates, which are already close to zero. So while many banks have an abundance of core deposits, their ability to reduce the price of these funds to protect their margin is limited. Since December 2000, the number of banks at risk to fallings rates has increased from 51% to 62%. Over that same time frame, the magnitude of risk has worsened as well. In December 2000, the average Margin at Risk was -4.71%. For third quarter 2002 the average margin at risk is -5.64%. Surprise! While it is hard to predict what effect the rate drop will have on the

overall economy, we can expect many banks’ net interest income to decline

during the last quarter of this year. The impact will likely be greater on

smaller institutions since they rely more on retail (core) deposits. How

long will this last? Will rates fall further, or begin to rise? Most

community banks are positioned to take advantage of rising rates, how long

will it be before this position pays off? 1 FDIC Quarterly Banking Profile, Commercial Banking Performance, Third Quarter 2002 |

|

This

A/L BENCHMARKS Industry Report article was published |

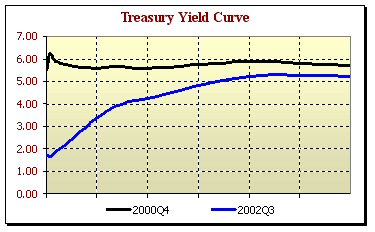

Short-term and long-term rates have been through some amazing changes

since December 2000. The most dramatic shift was the 475 basis point drop in

short-term rates. By December 2001 the Fed had lowered its discount rate

from 6.00% to 1.25%. Long-term rates have shifted significantly as well.

After briefly rising in first quarter of 2002, long-term rates have now

reached historic lows. The average conventional mortgage rate for third

quarter 2002 was 6.289%, the lowest it has been in thirty years.

Short-term and long-term rates have been through some amazing changes

since December 2000. The most dramatic shift was the 475 basis point drop in

short-term rates. By December 2001 the Fed had lowered its discount rate

from 6.00% to 1.25%. Long-term rates have shifted significantly as well.

After briefly rising in first quarter of 2002, long-term rates have now

reached historic lows. The average conventional mortgage rate for third

quarter 2002 was 6.289%, the lowest it has been in thirty years.  mpact on IRR position…

mpact on IRR position…