|

4th Quarter 2001 |

Interest Rate Risk, stable for the short-term, elevated for the

long-term

|

||||

|

|

|

Along with shrinking margins and major declines in credit quality, the

banking industry has one more worry to contend with: Long-term Interest Rate

Risk is rising. The last time this occurred was more than two years ago,

when banks showed a 3% annual increase in their EVE at Risk during the first

three quarters of 1999. Now, at the end of 2001, banks are showing a similar

trend.

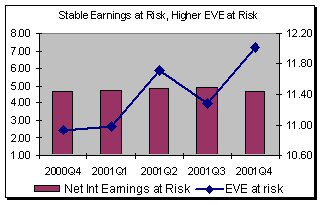

From the end of December 2000 to the end of December 2001 bank’s Net Interest Earnings at Risk (short-term risk) remained fairly stable moving only from 4.71 to 4.69. The change in EVE at risk (long-term risk) was much more pronounced moving from 10.93 up to 12.02%. What are some reasons for the increase? First, interest rates have dramatically changed stretching the industry’s ability to maintain adequate Net Interest Margin. And second, banks are beginning to lengthen their portfolios apparently to obtain better yields. Reacting to the margin squeeze. There was however one bright spot for NIM during the past year. The average NIM increased from 3Q to 4Q, it went from 4.28 to 4.30. One reason for the slight quarterly increase appears to be the lower rate banks are offering on their interest bearing transaction deposits. Interest bearing transaction deposits are money market accounts, NOW and savings accounts. Money markets (and some NOWs) are rate sensitive, and their average rates have declined with market rates over the year: 3.55, 3.11, 2.92, to end with 2.63. The rates on NOW and savings moved down at a much slower rate: 2.71, 2.70, 2.58, ending the year at 2.37. These type of accounts usually have administered rates (set by the bank, not by the market), and in many cases these rates don’t change much. To preserve some margin it appears that bankers have finally adjusted these rates down. . Unfortunately this may be one of the few tools that banker’s have left to prop-up net interest margin until the markets begin to move. Let the yield chasing begin

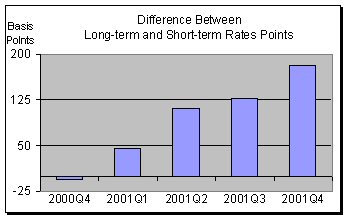

Banks appear to be reacting to the new rate environment just like they did back in the third quarter of 1999. To combat dwindling net interest margins, banks are starting to extend their asset maturities to reach for higher spreads. In the process, the longer asset duration may expose banks to shrinkage in market and economic values if market rates begin to rise. Is your board prepared? How is your bank handling the current interest rate environment? Are you prepared for what many believe will be an up turn in interest rates? Are you addressing the issue of short-term earnings, and taking more long-term risk to your institutions economic value? If so, are you being compensated for the risk? |

|

This

A/L BENCHMARKS Industry Report article was published |

Interest rate risk (IRR) is viewed in both a short-term and a long-term

perspective. To look at short-term IRR we look at Net Interest Earnings at

Risk, to look at long-term IRR we look at EVE at Risk.

Interest rate risk (IRR) is viewed in both a short-term and a long-term

perspective. To look at short-term IRR we look at Net Interest Earnings at

Risk, to look at long-term IRR we look at EVE at Risk.  The average Total Asset Duration for banks has lengthened slightly from

1.75 last year to 1.80 by the end of fourth quarter 2001. The regulatory

measure “Long-term Assets to Total Assets” has also increased over last

year, from 19.40 up to 19.93

The average Total Asset Duration for banks has lengthened slightly from

1.75 last year to 1.80 by the end of fourth quarter 2001. The regulatory

measure “Long-term Assets to Total Assets” has also increased over last

year, from 19.40 up to 19.93